In many African households, death and money are taboo topics rarely discussed, leave alone planned for. This is why the majority of lack any concrete succession plan when they die.

However, for married couples with a succession plan, in case of death or incapacitation, sharing of benefits reveals a skewed pattern that rarely favours men.

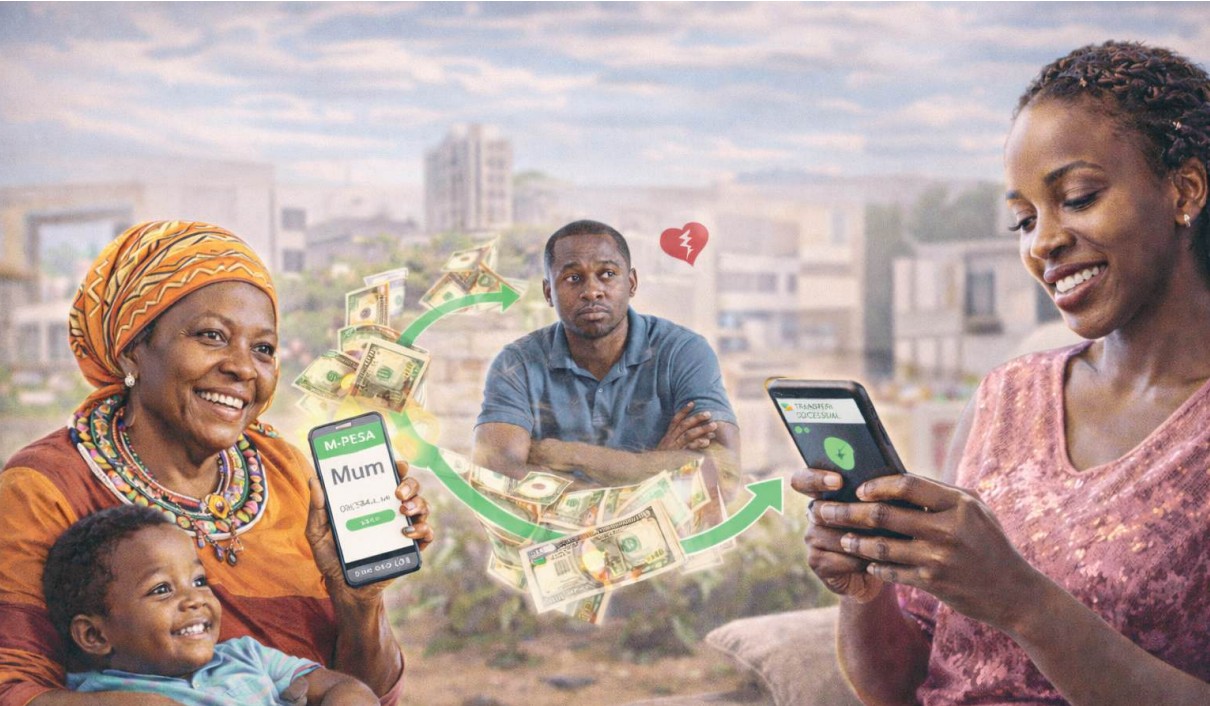

According to industry data, only one in 10 married women in Kenya chooses to transfer her benefits to her spouse. Instead,they channel the benefits to their mother, sisters or children.

The Retirement Benefits Authority says that only about 10 per cent of women list their husband as the primary beneficiary.

A majority nominate their mothers, sisters or children to take over the financial benefits in case a misfortune befalls them. Unity in marriage appears to stop at the doors of retirement or insurance benefits.

In sharp contrast, men overwhelmingly choose their wives, with about 95 per cent putting their wives as beneficiaries in case of any eventuality.

This trend, the authority says, is rooted partly in mistrust and partly in persistent myths surrounding retirement benefits.

“Many women fear that if they die, their accumulated wealth may end up being enjoyed by another woman,” said RBA assistant director, research strategy and planning, Monica Were.

“Others believe that nominating a husband could reduce the likelihood of the benefits reaching their biological children, misconceptions the regulator is working to dispel.”

The data paint a scenario where men appear more confident entrusting their wealth to their partners than women do.

Analysts from insurance benefits providers, sociologists and some women the Star Interviewed reveal a belief that men are naturally polygamous.

Among the top concerns that a man may not be the one to enjoy the wife’s benefits is that women worry that their husbands may secretly have other partners or children.

Only when a man is buried with no other woman emerging to claim property do some wives feel assured of his fidelity.

This suspicion leads many women to avoid risking their children’s inheritance.

The RBA notes that this trend is mainly driven by misinformation spread informally and becomes embedded over time.

For instance, many scheme members believe that nominating parents or siblings shields their savings from potential misuse by a spouse.

Yet under Kenyan law, the primary role of a beneficiary nomination is to guide trustees on who should receive the benefits should the member die. It does not take away a spouse’s legal rights nor does it alter ownership during the member’s lifetime.

Still, the emotional, cultural, and relational dynamics continue to shape choices.

“These decisions reflect deep-seated beliefs around money, trust and family. But they also highlight an urgent need for consistent retirement literacy,” Were said during a session with business journalists.

The findings that covered retirement planning and other benefits like insurance payouts come at a time when Kenya is grappling with broader challenges in retirement planning.

Despite steady growth in membership and pension assets, only 26 per cent of workers in the country are covered by a formal pension scheme.

The majority, especially those in the informal sector, are left vulnerable, increasing the risk of old-age poverty.

RBA data shows that pension assets have grown consistently and are projected to hit Sh3.2 trillion by the end of the authority’s 2024–2029 strategic period.

Even so, the regulator says low coverage and widespread myths continue to undermine the effectiveness of the retirement benefits framework—beneficiary nomination being one of the most misunderstood components.

According to the authority, a significant number of Kenyans mistakenly believe that naming a beneficiary automatically transfers ownership of the retirement funds to that person, even while the contributor is still alive.

“Others assume that spouses will automatically inherit benefits without formal nomination, an error that has, in many cases, led to lengthy and expensive succession battles,” Were added.

Were argued that failing to nominate beneficiaries or nominating them based on fear rather than strategy can derail family finances.

In the absence of a legally recognised beneficiary, retirement benefits are subjected to lengthy legal processes, which can delay payouts. For families relying on a deceased member’s pension to cover urgent expenses, these delays can be devastating.

The RBA urges Kenyans to update their beneficiary information regularly—especially after major life events such as marriage, divorce, childbirth, or the death of previously nominated individuals.

To address the widespread misconceptions, the authority is ramping up its awareness campaigns and advocating for policy changes.

Among its recommendations is mandatory retirement training earlier in employees’ working lives, stricter enforcement of benefit preservation rules, and expanded education targeting informal-sector workers.

Octagon Africa group CEO Fred Waswa says this is a common occurrence due to lack of trust that the husband will take care of the benefits well in the interest of the children and a belief that upon death the husband will quickly marry another wife and enjoy her sweat.

“So they end up nominating either their parents or sisters to be guardians of the benefits in the event of death," Waswa said.

“In our experience, both routes of either nominating a husband or siblings has its pitfalls. We at Octagon have tried to address this for our members by providing them the route of a children’s trust.”

He adds that with a trust the nominated beneficiary will earn a trust which she can set up while alive and the trust then manages the funds professionally and upkeep and other costs are paid without being exposed to abuse.

Sociology lecturer at Daystar University Kennedy Ongaro said that many women believe that if they die, their children could be treated as second-class family members, especially if their husbands remarry.

To ensure the children’s welfare, women prefer naming their mothers, who share a blood relationship with them and whom they trust to protect their offspring.

The principle of “blood is thicker than water” plays a crucial role. Mothers and siblings feel safer than husbands who, unlike children or parents, share no blood ties.

Ongaro notes that many modern marriages face increasing tension, infidelity and conflict.

The media, he says, amplifies stories of domestic disputes, inheritance battles, and remarriages, influencing women to prepare for worst-case scenarios.

“In some communities, women face subtle or overt pressure to bear sons. If a woman has only daughters—or struggles with infertility - the marriage may seem less secure. In such circumstances, a woman is unlikely to designate her husband as a beneficiary,” Ongaro said.

Ongaro emphasised that strained relationships with in-laws heavily influence beneficiary choices.

In cases where in-laws have a history of mistreating widows or attempting to seize property, women avoid giving husbands control over their assets to shield their children from extended family battles.

“In certain cultures, women are traditionally excluded from decision-making or inheritance discussions. Ironically, these same norms discourage women from trusting their spouses with their assets,” the lecturer added.

“Religious beliefs can also influence who is considered a rightful heir, shaping women’s choices.”

Kenya has witnessed many high-profile inheritance cases. Last year, a new legal battle broke out within the family of the late powerful politician Peter Mbiyu Koinange over a prime piece of land in Nairobi’s Central Business District, valued at Sh2.4 billion.

His widow Margaret Njeri and daughter Lennah Catherine took legal action against fellow widow Eddah Wanjiru and her daughter Fiona Mbiyu, accusing them of mishandling the property and placing it at risk of being sold due to unpaid county rates.

The High Court in Eldoret also annulled a contested will that was being used to distribute a massive estate (worth over Sh3.5 billion) of a former chief in Elgeyo Marakwet and Uasin Gishu.

The will favoured the second wife but was found to have forged signatures. The court declared it null and void

In February 4, 2026, the Court of Appeal upheld a ruling recognising a customary trust in favour of widow Mary Mwangi, affirming her right to a portion of a seven-acre property in Thika previously held in trust by her deceased husband’s brother.

Delivering the judgment on January 30, a three-judge bench dismissed an application to review the 2025 Environment and Land Court decision, confirming that Mary was the rightful beneficiary of a portion of a seven-acre property, which was held in trust for her deceased husband Joseph Mwangi by his brother.

The family of the late former ECK chairman Samuel Kivuitu has also been embroiled in a bitter fight over his Garden Estate property. His second wife and children from different marriages differ on whether the property is matrimonial (for the widow) or should be shared among all heirs.

“In polygamous unions, a woman may worry that her assets will benefit the children of another wife. For second wives, the fear is especially strong, since the first wife’s children typically enjoy higher status or earlier claims,” Ongaro says.

The lecturer observes that divorced friends, acquaintances, or relatives often share cautionary stories that erode married women’s confidence. These narratives of betrayal or loss reinforce fears and contribute significantly to the trend.

Taken together, these factors paint a picture of growing insecurity within marriages. Women appear to view their external families’ mothers, sisters, and children, as safer guardians of their assets than their spouses.

Comments 0

Sign in to join the conversation

Sign In Create AccountNo comments yet. Be the first to share your thoughts!