Global ratings agency S&P recently upgraded Kenya’s long-term sovereign credit rating from ‘B-’ to ‘B’.

It cited improved foreign exchange reserves, stronger diaspora remittances, and robust export earnings that have eased pressure on the shilling and reduced short-term liquidity risks.

According to the agency, the outlook remains stable, signaling that while Kenya faces fiscal challenges, its economy is showing resilience and growth momentum.

“The upgrade reflects our view that Kenya’s near-term external liquidity risks have receded. External data revisions, coupled with strong performances in coffee exports and diaspora remittances, supported a narrowing of Kenya’s current account deficit to 1.3% of GDP in 2024, from 2.6% in 2023," S&P said in a statement.

President William Ruto has projected economic growth at 5.6% in 2025, above both Treasury and Central Bank estimates.

With the economy expanding faster than last year’s 4.7%, the ratings boost provides Kenya with a credibility lift in international markets.

But what exactly is a credit rating and why does it matter for ordinary Kenyans?

What is a credit rating?

A credit rating is like a financial “report card” for a country, company, or institution.

It measures the ability of a borrower to repay debt on time.

Just as individuals are assigned credit scores by banks, sovereign credit ratings assess the risk of lending to a government.

For Kenya, this rating tells international investors, lenders, and bond markets how risky or safe it is to lend money to the government.

A higher rating generally means lower borrowing costs and stronger investor confidence.

S&P Global Ratings is an American credit rating agency (CRA) and a division of S&P Global that publishes financial research and analysis on stocks, bonds, and commodities.

It is one of the world's "Big Three" leading and most reputable credit rating agencies. Others are Moody's Ratings and Fitch Ratings.

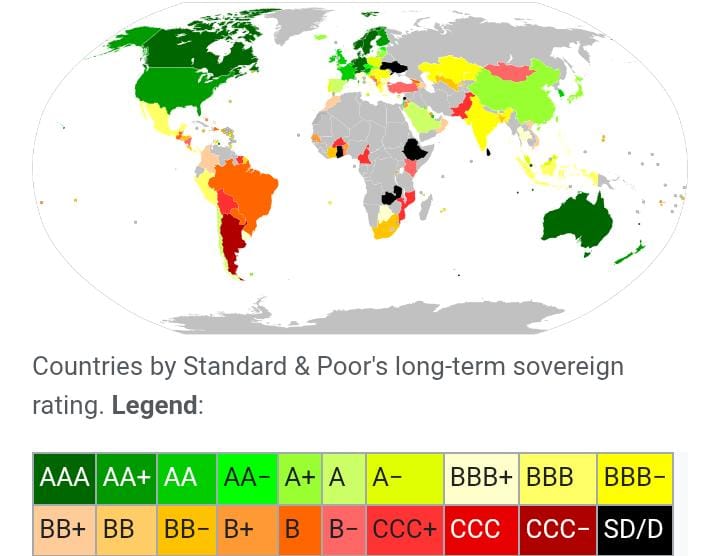

These three dominate the market and their reports influence everything from interest rates on loans to the success of Eurobond sales. S&P rates borrowers on a scale from AAA to D.

Intermediate ratings are offered at each level between AA and CCC (such as BBB+, BBB, and BBB−).

For some borrowers issuances, the company may also offer guidance (termed a "credit watch") as to whether it is likely to be upgraded (positive), downgraded (negative) or stable.

How the rating scale works S&P uses a scale ranging from AAA (highest quality) to D (default).

Ratings are divided into two broad categories:

1. Investment Grade- Seen as relatively safe (AAA to BBB).

2. Speculative or “Junk” Grade- Higher risk but higher potential returns (BB to D).

Kenya’s new rating of ‘B’ falls under the speculative grade, meaning the country is still considered risky but has shown enough resilience to avoid immediate default pressures.

This ‘B’ means that Kenya has the capacity to meet its financial commitments for now, but could be vulnerable if economic or financial conditions worsen.

Why Kenya was upgraded

According to S&P, the decision to upgrade Kenya’s rating was informed by a combination of positive economic developments.

Diaspora remittances remained a key pillar, with Kenyans abroad sending home over $4.3 billion last year, a flow that significantly strengthened the country’s foreign exchange reserves.

At the same time, strong export performance in tea, horticulture, and growing service industries such as ICT and tourism provided steady inflows of foreign currency.

The shilling, which had faced turbulence in 2023–24, has also shown signs of stability, easing pressure on external balances.

In addition, Kenya successfully restructured some of its external obligations, improving its short-term liquidity outlook by buying time on upcoming repayments.

These improvements collectively outweighed persistent challenges, including high interest costs, a public debt stock above 65 percent of GDP, and the slow pace of fiscal consolidation.

Interior Principal Secretary Raymond Omollo has welcomed the rating noting recognition showed Kenya was steadily regaining global confidence while delivering tangible benefits for its citizens.

“This is a strong endorsement of President William Ruto’s leadership and economic reforms,” he said.

Why credit ratings matter

A sovereign credit rating carries real-world consequences that directly affect a country’s economy.

When Kenya issues Eurobonds, the level of interest demanded by investors is influenced by the rating, meaning an improved score can reduce borrowing costs.

Foreign investors also rely heavily on these ratings to gauge risk before committing funds to government securities or local projects, so an upgrade strengthens confidence in the market.

Currency stability is another area affected, as ratings shape perceptions of risk: a downgrade often weakens the shilling, while an upgrade supports its stability.

The private sector is not immune either, since local banks and companies that borrow internationally often face rates linked to the sovereign rating.

In essence, a stronger credit rating allows Kenya to borrow more affordably and attract greater investment, advantages that ultimately filter down to businesses and households through improved financial stability and economic opportunities.

The latest rating shows that Kenya is competitive regionally, though still some distance from achieving an investment grade like Botswana (BBB+).

A year ago, the agency downgraded Kenya’s rating from B to B- citing the repeal of the Finance Bill 2024-25, arguing it would slow the fiscal consolidation.

In July, Moody’s also downgraded its rating to junk status, while Fitch also downgraded it to B- from B.

It comes at a time the IMF board is set to sit to approve $600 million disbursement under Kenya’s $3.6 billion lending programme, which expires next year.

Risks that remain

Despite the recent upgrade, Kenya still faces several economic headwinds that could undermine its outlook.

Debt servicing obligations remain a key concern, with looming Eurobond maturities expected to strain public finances.

At the same time, fiscal pressures are mounting as tax revenues continue to fall short, even as government spending remains high.

Externally, the economy is vulnerable to global shocks, rising US tariffs, higher oil prices, and escalating geopolitical tensions all pose risks to exports, remittances, and investor sentiment.

On the domestic front, political uncertainty or instability could further dampen confidence and delay much-needed reforms, complicating efforts to sustain economic momentum.

S&P’s stable outlook means no immediate changes are expected, but progress on fiscal reforms and debt management will determine future movements.

What it means for ordinary Kenyans

Improved credit ratings can offer several advantages for Kenya’s economy.

Lower borrowing costs ease pressure on the government to introduce new taxes, while a more stable shilling helps reduce the cost of imports like fuel, helping to keep inflation in check.

A better-rated business environment also enhances investor confidence, encouraging capital inflows that support job creation and economic growth.

Meanwhile, local banks may find it easier to access foreign capital, potentially translating into more affordable loans for businesses and consumers.

However, these gains remain fragile. Without meaningful reforms to boost revenue and manage public spending, continued debt accumulation could reverse progress and push the country back into financial distress.

For Kenya to climb further up the ratings ladder, it must strengthen revenue collection and reduce reliance on borrowing and manage debt repayments carefully, especially Eurobonds.

It must also diversify exports beyond tea and horticulture and maintain political stability and consistent policy reforms.

The S&P upgrade is a vote of confidence, but it is also a reminder that Kenya must sustain reforms and fiscal discipline.

For now, it gives the government some breathing space and a stronger hand in global financial negotiations.

Comments 0

Sign in to join the conversation

Sign In Create AccountNo comments yet. Be the first to share your thoughts!