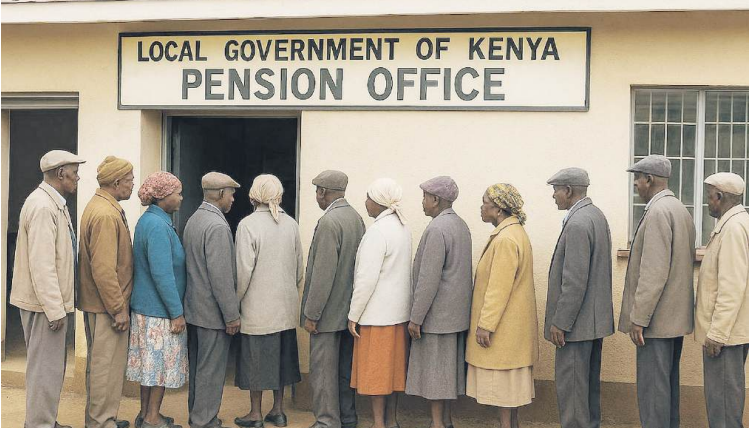

For years, Kenyan workers saving for retirement have watched inflation, high interest rates and a weakening shilling chip away at the value of their old age investments.

A volatile market environment due to inflation, rising interest rates and a weakening shilling have in the past two years, eaten into pension fund returns.

However, fresh data suggests 2025 may finally be the year when savers get some breathing space.

In the 12 months to June 2025, the pension schemes recorded a median return of 30 per cent, compared to inflation of just 3.8 per cent.

That translates into a real gain of 26.2 per cent for pension members—a turnaround from recent years when savings barely held their value.

Pension savers are set to reap big after their funds recorded the highest annual returns in 12 years, backed by a good performance from equities and fixed income investments, government securities and diversification into offshore markets.

The latest Zamara Consulting Actuaries Schemes Survey shows that, in 2022 and 2023, inflation hovered near 7.9 per cent while pension returns lagged at 0.8per cent and 6.6per cent respectively.

“This year’s performance is a reminder that disciplined investing, diversification, and a long-term perspective can deliver real value to pension members,” said Zamara Group CEO Sundeep Raichura.

The latest Zamara Consulting Actuaries Schemes Survey (Z-CASS), covering 407 retirement schemes with more than Sh1.3 trillion in assets, shows pension funds delivering their strongest performance in years, with returns that not only kept up with inflation but surged well ahead of it.

Despite the schemes championing for increased diversification, data by the Retirement Benefits Authority shows that a significant portion, 92 per cent, of pension assets still remained concentrated in four key asset classes: government securities, guaranteed funds, quoted equities and immovable property.

These traditional investment avenues have long been favored for their perceived stability and predictable returns, constituting 94.8 per cent of total pension assets across the six primary investment categories.

According to Zamara, the surge was powered by robust performance in local equities (50.7 per cent) and government bonds (27.8 per cent), which together lifted fund portfolios.

Over three years, pension schemes delivered an annualised return of 16.4 per cent, again comfortably ahead of the 5.4 per cent inflation rate.

Even over five years, schemes grew by an average of 13 per cent annually, compared to inflation at 6.1 per cent, giving savers a meaningful cushion.

Zamara Group head of asset consulting Neha Datta says that pension schemes should focus on diversification and view retirement benefits from a long-term perspective.

“Pension schemes need to remain attuned to asset class behaviour, regulatory developments and risk-adjusted strategies to support sustainable outcomes for their members over time,” said Datta.

Industry data by RBA shows that Kenya’s pension schemes significantly reallocated their portfolios over the past year, with investments in government securities surging by 46 per cent on the back of attractive interest rates.

Quoted equities (trading on shares of listed companies) also registered strong growth, rising 42 per cent amid a rebound in the stock market, particularly in the final quarter of the year.

In contrast, allocations to immovable property and fixed deposits contracted sharply by 25 per cent, pointing to a shift away from less liquid and lower-yielding assets.

Cash holdings similarly fell by 33 per cent as schemes moved to capture better returns in government debt and equities.

The investment trends highlight pension funds’ growing preference for liquid, higher-yielding assets, even as traditional havens like property and deposits lose appeal.

Offshore investments also proved their worth, emerging as the top-performing asset class over the 3-year (22.2per cent) and 5-year (13.9per cent) periods.

Yet uptake remains limited, with only 190 schemes allocating an average of two per cent to global markets, leaving much untapped potential for diversification.

However, the report points out that not all strategies paid off equally. While moderate and aggressive schemes posted higher short-term gains thanks to equities, it was the conservative schemes, heavily invested in government bonds, that had the edge over five years.

Their steady growth averaged 13.1 per cent annually, highlighting the value of stability in volatile times.

Offshore investments cushioned some of the blow, but limited exposure meant most savers did not fully benefit from dollar strength.

Despite the defined contribution pension schemes posting a 30 per cent return over the past 12 months, industry experts caution that not all the gains will be available for distribution to members.

Regulations exclude unrealised gains and losses from fair value assessments when calculating distributable income.

This means schemes may record lower effective payouts depending on their portfolio structure and the extent to which returns have been realised.

“The findings emphasise not just the strong recent returns, but also the importance of diversification and viewing retirement benefits from a long-term perspective,” Datta said.

“Pension schemes need to remain attuned to asset class behaviour, regulatory developments, and risk-adjusted strategies to support sustainable outcomes for their members over time.”

A separate report by RBA shows that benefits assets are expected to continue their growth trajectory in 2025, driven by sustained member contributions, particularly with the ongoing increase in NSSF contributions.

"Interestingly, alternative asset classes are increasingly gaining attention as avenues for diversification. While uptake has been historically slow due to perceived uncertainties, the past year saw notable growth in several areas," RBA noted on its latest report.

Furthermore, anticipated investment income from fixed-income investments and the continued rebound of the stock market are expected to further fuel this expansion.

The growth comes at a time that the government is planning to tap on the insurance funds to develop mega projects.

A team picked by the National Treasury to help the government unlock the potential of local investors in funding PPP projects says that the long-term investment nature of pension and insurance funds makes them ideal for the power lines project.

Treasury principal secretary Chris Kiptoo said that the funds are already attracting interest, with Ketraco keen to conclude PPP deals to fund the construction of electricity lines and help boost the country's electricity supply without relying on loans.

"Ketraco is well-suited for pension funds and insurance companies due to predictable cash flows," said Kiptoo earlier in the year.

Comments 0

Sign in to join the conversation

Sign In Create AccountNo comments yet. Be the first to share your thoughts!